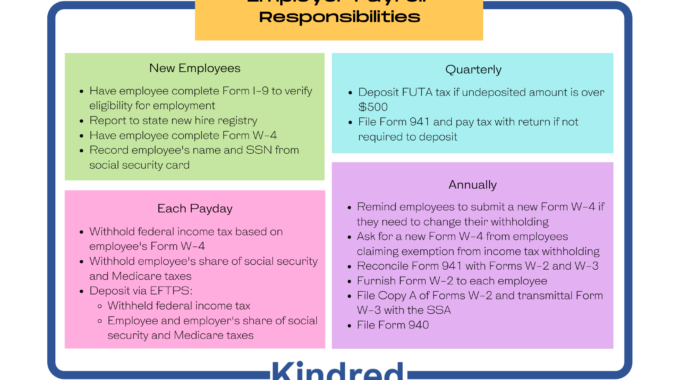

These days, it seems like everyone has an online presence. Whether it's Facebook, Twitter, Instagram, YouTube, TikTok, or just plain old websites, everybody has a…

If your company has a 401(k) plan, you know it’s a great benefit for your employees. Payroll deduction is an easy way to save for retirement, and can provide a tax-advantaged way to grow that important nest egg.

If your company has a 401(k) plan, you know it’s a great benefit for your employees. Payroll deduction is an easy way to save for retirement, and can provide a tax-advantaged way to grow that important nest egg.

But you also know that 401(k) plans come with some critical compliance issues. Both the IRS and Department of Labor (DOL) regulate employee benefit plans, so it’s important to stay within the lines. Here are two common errors to avoid in your plan’s administration.

Deposit contributions timely.

Here’s the rule: When you withhold 401(k) contributions from employee paychecks, you must deposit them into employee accounts as soon as administratively feasible. That means there isn’t a specific number of days after a payroll run, but rather as soon as you can “reasonably segregate” those contributions and make the deposit. It’s similar to the timing of payroll tax deposits – the IRS figures if you can deposit FICA/Medicare and tax withholding within just a few days after payday, you can do the same with 401(k) deductions.

The penalties for making late deposits can be steep, including the possibility of plan disqualification if it’s a recurring issue. At the very least, the employer must deposit late contributions along with any missed earnings.

So it’s important to look at your payroll process and see if you need to tighten it up to avoid this issue. If you want to read more about the deposit rule, click here.

Follow the plan document’s definition of employee compensation.

Do you know where your 401(k) plan document is? You might not have looked at your plan document since you signed it many years ago. But now’s a good time to unearth it, dust it off, and look for the section titled “Compensation” to ensure you’re not missing something.

We generally think of compensation in terms of cash paid to an employee, but it can also include some non-cash items. Here are some elements that make up compensation:

- Wages, including overtime

- Bonuses

- Commissions

- Tips

- Fringe benefits

Your plan document will specify which of these items should be used for employee contributions, discrimination testing, and the allocation of any employer contributions. The definition can get complicated pretty quickly! If your plan has a complicated definition of compensation, you might need to develop a worksheet to calculate the correct amounts.

Your plan’s definition of compensation must be non-discriminatory, which means that highly compensated employees can’t benefit to a greater degree than rank and file employees. For example, if your plan excludes overtime from the definition of compensation, that could reduce the benefit for hourly employees while providing a greater benefit to salaried employees.

Visit with your 401(k) plan’s third party administrator if you have questions about your plan. To read more from the IRS on this issue, click here.

Related Posts