These days, it seems like everyone has an online presence. Whether it's Facebook, Twitter, Instagram, YouTube, TikTok, or just plain old websites, everybody has a…

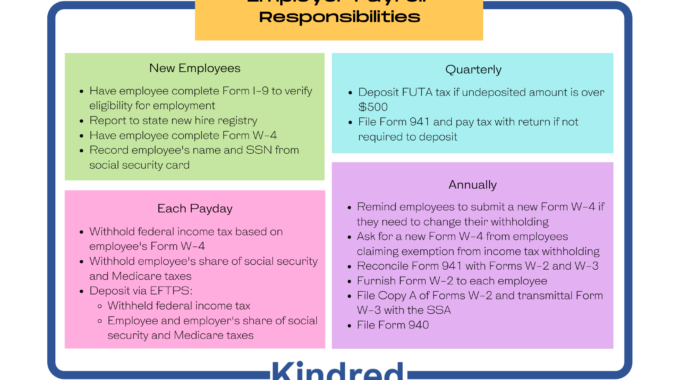

Year-end brings lots of payroll considerations to the forefront. Regardless of whether Kindred CPA processes your payrolls or you do it in-house, if you provide any of the following benefits, you’ll need to gather this information to properly account for taxable income on W-2’s:

Group Term Life Insurance

Group Term Life Insurance

If you pay group term life insurance premiums for yourself or your employees and the face amount of the policy is over $50,000, a portion of the cost of the insurance must be included in the W-2’s (Box 12, Code C) for affected employees. This also applies to spouse or dependent coverage with a face amount over $2,000. To calculate this “imputed income”, use the Premium Table on page 15 of IRS Publication 15-B.

Life Insurance Other Than Group Term

If the company pays whole life or non-group life insurance premiums for owners, employees, spouses or dependents, and the corporation is neither the policy owner nor the beneficiary, this may need to be added to W-2’s.

S-Corporation Shareholder Benefits

Certain fringe benefits (health insurance, disability, long term care and group term or single life insurance premiums) paid by the company on behalf of a more than 2% shareholder must be included on the W-2 in Box 1 as taxable wages. This may also apply to any benefits for the shareholder’s spouse, children, grandchildren, or parents.

Bonuses, Trips, Awards and Prizes

All gifts of cash, gift certificates, gift cards, stock in a corporation, merchandise, trips, awards, and prizes are taxable to the employee and must be included in the W-2. There is an exception for gifts that are considered to be de minimis, which is any property or service you provide to an employee that has so little value that accounting for it would be unreasonable or administratively impracticable. Both the frequency and value of the gift determine whether or not it is de minimis. Examples include:

- Holiday or birthday gifts other than cash with a low fair market value

- Flowers or fruit provided to employees under special circumstances (such as illness, family crisis, or outstanding performance)

- Occasional parties or picnics for employees and their guests

- Occasional tickets for theater or sporting events (but not season tickets)

- Coffee, doughnuts, soft drinks

But remember – gifts of cash or cash equivalents are always reportable, regardless of the value.

Employer Provided Vehicle

If your company provides a vehicle to an employee, the value of their personal use of the vehicle is taxable income to them and reportable on the W-2 in boxes 1, 3 and 5. Commuting (to and from home to the workplace) is considered personal use. The IRS requires mileage logs to prove business use of the vehicle. See IRS Publication 15-B, page 25 for more information.

Group Health Insurance

If you offer employer-sponsored health insurance to your employees and you filed more than 250 Forms W-2 in the previous year, you are required to report the cost of health insurance provided to each employee on Form W-2 Box 12, Code DD.

Health Savings Accounts (HSA)

Form W-2, box 12, Code W requires reporting of any employer contributions (including amounts employees contribute using a Section 125 cafeteria plan) to an HSA. This also includes 2% shareholders of S Corporations if they receive an employer paid HSA contribution. Employee contributions are pre-tax only if they’re made through a cafeteria plan.

Dependent Care Assistance Program (Sec. 129)

The American Rescue Plan Act (ARPA) allowed the amount of nontaxable dependent care benefits to be increased from $5,000 to $10,500 for calendar year 2021. This provision applies as long as the dependent care plan was amended timely. An employer may exclude from income the lesser of $10,500, the employee’s earned income for the year, or the earned income of the employee’s spouse for the taxable year for a dependent care plan. The benefit is limited to $5,250 for your employees who are married but filing a separate tax return from their spouse. The total amount of dependent care benefits must be reported separately on the employee’s W-2 in Box 10.

More information on dependent care assistance programs and the impact of pandemic relief can be found on the IRS website by clicking here.

Business Expense Reimbursements

In general, if your company reimburses employees for actual travel and non-entertainment related meal expenses, and employees provide written substantiation of actual expenses, there is no additional reporting requirement on the employee’s Form W-2. However, if your company provides a per diem or allowance without written substantiation by the employee and/or the employee does not return any excess amounts, the excess amount is reported as taxable wages in Box 1 of Form W-2.

Car Allowances

Flat rate car allowances where the employee does not submit substantiation for the business purpose of each trip are considered taxable to the employee and must be included on the employee’s W-2. There is an exception if your allowance for the employee is less than or equal to the appropriate federal rate, in which case it is not considered taxable compensation. For more information, see IRS Publication 535, Business Expenses, page 44.

Qualified Moving Expense Reimbursements

Qualified moving expenses reimbursed by an employer are included in the employee’s income in accordance with the Tax Cuts and Jobs Act (TCJA) of 2017.

Moving expenses are still deductible for active duty members of the Armed Forces who move pursuant to a military order, therefore those expenses reimbursed by the employer would be excluded from wages.

Interest-Free Loans (Sec. 7872)

An interest-free loan (or loan below market interest rate) in excess of $10,000 by an employer to an employee is treated as wages to the employee to the extent of the differences between normal market interest rate and the rate payable by the employee over the term of the loan. (Debt forgiveness is also considered compensation for an employee.)

Educational Payments or Reimbursements

Certain educational assistance benefits that an employer provides to an employee may need to be included in the employee’s taxable income and included on the W-2. The guidelines are specific; please contact our office for assistance to determine if your situation is taxable or non-taxable.

Athletic Club and Country Club Dues

If your company pays dues on behalf of your employees for athletic clubs or country clubs, include it on the employee’s W-2.

Nonqualified Deferred Compensation Plans

Contributions must be reported on employee’s W-2. See the W-2 instructions, page 12 for more information.

Retirement Plans

“Elective deferrals” are sometimes called “salary reduction contributions” and refer to an employee’s election to defer some of their income to a retirement plan on a pretax basis. Because this election reduces an employee’s taxable income, it’s reportable on the W-2 in Box 12, with a code identifying the type of plan:

- Elective deferrals under a 401(k) plan are reported in Box 12, Code D

- Salary reduction contributions under a SIMPLE plan are reported in Box 12 with Code S unless the SIMPLE plan is part of a 401(k) arrangement, in which case use Code D.

- Elective deferrals under a section 403(b) plan use Code E

- Elective deferrals under a section 408(k)(6) salary reduction SEP use Code F

- Elective deferrals and employer contributions to any 457(b) deferred compensation plan use Code G unless amounts are subject to a substantial risk of forfeiture

For information on employee benefit or retirement plan contribution limits for 2021, please refer to our blog post on 2021 Dollar Limits. We will be posting 2022 limits shortly once updated mileage rates have been released.

Third-Party Sick Pay

Sick pay provided under a separate plan may be subject to federal income, FICA, FUTA and SUTA taxes. Either you or your third-party payer should deposit and report sick pay on employee W-2’s. If your third party payer does not do this on your behalf, they must report sick pay amounts to you regularly so you can make timely payroll tax deposits. They are also required to provide an annual statement of payments no later than January 15. Please contact us prior to December 31 if Kindred CPA processes your payroll and you have employees collecting sick pay from a third party so we can gather the appropriate information prior to completing Form W-2.

Form 8922 Third Party Sick Pay Recap must be completed by either the third-party payer or the employer, depending on the type of arrangement you have with the third-party payer.

Questions?

If you have further questions, give us a call at (785) 842-8844. We’re here to help you navigate year-end!

Related Posts